What is autoregressive distributed lag approach?

What is autoregressive distributed lag approach?

1. Are standard least squares regressions that include lags of both the dependent variable and explanatory variables as regressors. It is a method of examining cointegrating relationships between variables.

What is autoregressive distributed lag ARDL?

An autoregressive distributed lag (ARDL) model is an ordinary least square (OLS) based model which is applicable for both non-stationary time series as well as for times series with mixed order of integration.

What is the difference between autoregressive model and distributed lag model?

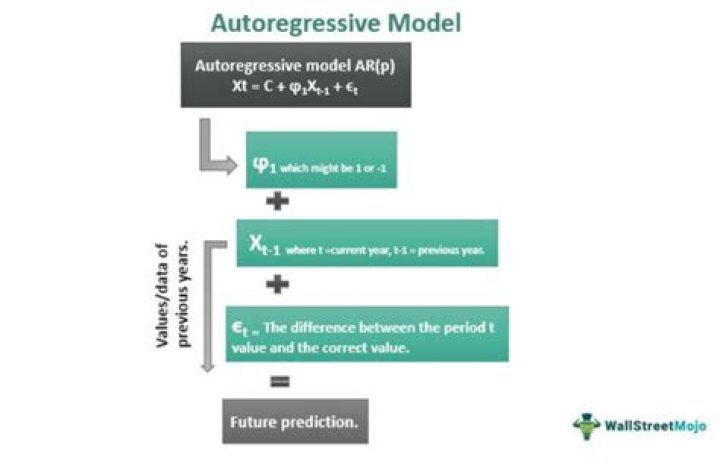

If the model includes one or more lagged values of the dependent variable among its explanatory variables, it is called an autoregressive model. Distributed Lag (DL) Models: These models include the lagged values of the explanatory variables.

What is the purpose of ARDL model?

The ARDL / EC model is useful for forecasting and to disentangle long-run relationships from short-run dynamics. Long-run relationship: Some time series are bound together due to equilibrium forces even though the individual time series might move considerably.

What is meant by distributed lag model?

Distributed-Lag Models. A distributed-lag model is a dynamic model in which the effect of a regressor x on y occurs. over time rather than all at once.

Why we use distributed lag model?

In statistics and econometrics, a distributed lag model is a model for time series data in which a regression equation is used to predict current values of a dependent variable based on both the current values of an explanatory variable and the lagged (past period) values of this explanatory variable.

What is lag model?

What does ARDL mean?

Autoregressive-Distributed Lag

“ARDL” stands for “Autoregressive-Distributed Lag”. Regression models of this type have been in use for decades, but in more recent times they have been shown to provide a very valuable vehicle for testing for the presence of long-run relationships between economic time-series.

When would you use a distributed lag model?

In summary, the finite distributed lag model is most suitable to estimating dynamic rela- tionships when lag weights decline to zero relatively quickly, when the regressor is not highly autocorrelated, and when the sample is long relative to the length of the lag distribution.

What is Koyck approach?

Koyck has proposed an ingenious method of estimating distributed-lag models. Suppose we start with the infinite lag distributed-lag model (17.3. where X, such that 0 < X < 1, is known as the rate of decline, or decay, of the distributed lag and where 1 — X is known as the speed of adjustment.

Why we use autoregressive distributed lag model?

The autoregressive distributed lag model (ADL) is the major workhorse in dynamic single-equation regressions. Sargan (1964) used them to estimate structural equations with autocorrelated residuals, and Hendry popularized their use in econometrics in a series of papers1.

What does it mean to lag a variable?

A dependent variable that is lagged in time. For example, if Yt is the dependent variable, then Yt-1 will be a lagged dependent variable with a lag of one period. Lagged values are used in Dynamic Regression modeling.